3.3C - Sticky versus Flexible Wages and Prices

In macroeconomics there is both a short run and a long run. The short run is the time period in which at least one factor is fixed. For example, the price of inputs (hourly wages paid to labor and other unit resource prices) remains fixed, or sticky, in the short run. However, the price of firms’ output in the product markets varies directly with the price level. Input prices remain fixed for many reasons, e.g., wage contracts, menu pricing, and delays in recognizing unanticipated inflation. The lag between changes in output prices and changes in input prices results in firms earning short-run profits when there is inflation or losses when there is deflation. The long run in macroeconomics is the period of time in which input prices adjust to changes in the overall price level.

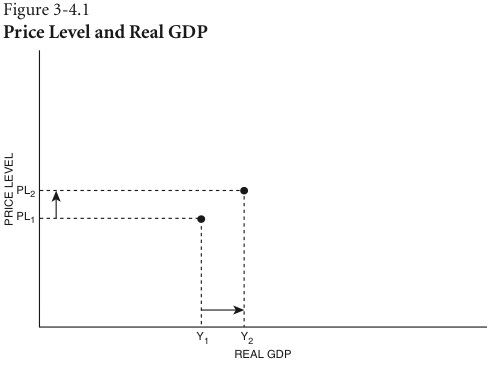

With price level increases, product market prices increase while factor market prices remain fixed. Fixed input prices and higher output prices leads to profit. This profit provides firms with an incentive to increase production. Refer to Figure 3-4.1. Notice that as price level increases from PL1 to PL2 that real gross domestic product (GDP) increases from Y1 to Y2.

The opposite would occur if product market prices fall with a decrease in the price level. Firms experience losses when input prices remain high and output prices decrease. The losses result in a decrease in production which leads to a decrease in real GDP.

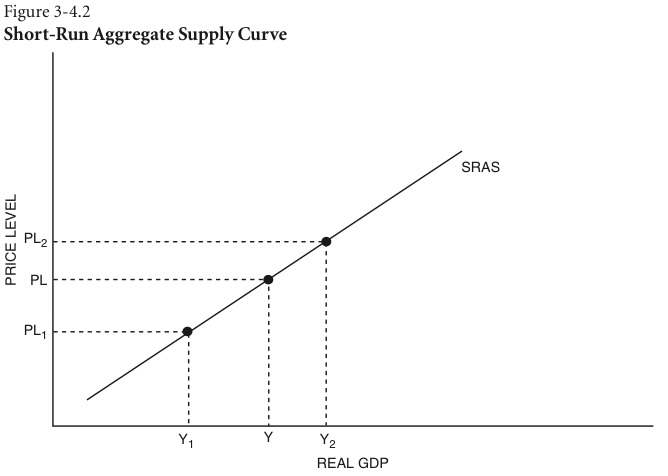

The result of firms varying their production directly with changes in the price level is an upward sloping AS curve in the short run. Hence, in the short run, the level of real GDP is directly related to the price level.

Figure 3-4.2 illustrates the SRAS.

|

|

|